728x90

german <- read.csv('German_credit.csv')

colnames(german)

[1] "ID" "Checking_account" "Duration_in_month" "Credit_history"

[5] "Purpose" "Credit_amount" "Saving_accout" "Present_employment"

[9] "Installment_rate" "Personal_status___sex" "Other_debtors_guarantors" "Present_residence"

[13] "Property" "Age" "Other_installment_plan" "Housing"

[17] "Num_of_existing_credits" "Job" "Num_of_people_liable" "Telephone"

[21] "Foreign_worker" "Credit_status"

table(german$Credit_status)

N Y

700 300 사용할 데이터는 German_credit 데이터셋입니다.

총 1000개의 관측치와 22개의 column으로 구성된 데이터입니다.

저희가 사용할 target 변수는 Credit_status이며, No가 700개, Yes가 300개를 포함합니다.

library(sampling)

stratified_sampling <- strata(german, stratanames = c("Credit_status"), size =c(300,300),

method="srswor")

st_data <- getdata(german, stratified_sampling)

table(st_data$Credit_status)

N Y

300 300 Class imblance 문제를 완화시키고자, sampling 패키지의 층화추출 함수 strata 를 사용합니다.

데이터 셋은 300개의 No와 300개의 Yes로 구성됩니다.

library(caret)

train <- createDataPartition(st_data$ID, p=0.7, list=FALSE)

td <- st_data[train,]

vd <- st_data[-train,]

다음으로, 데이터 분할을 진행합니다.

Train 데이터셋을 70%, Test 데이터셋을 30%로 분할합니다.

colnames(td)

[1] "ID" "Checking_account" "Duration_in_month" "Credit_history"

[5] "Purpose" "Credit_amount" "Saving_accout" "Present_employment"

[9] "Installment_rate" "Personal_status___sex" "Other_debtors_guarantors" "Present_residence"

[13] "Property" "Age" "Other_installment_plan" "Housing"

[17] "Num_of_existing_credits" "Job" "Num_of_people_liable" "Telephone"

[21] "Foreign_worker" "Credit_status" "ID_unit" "Prob"

[25] "Stratum"

td <- td[, -c(1,23,24,25)]

vd <- vd[, -c(1,23,24,25)]

column에 strata 함수에 의해서 생성된 3개가 새롭게 나타납니다.

필요없는 이 3가지 변수와 ID 변수를 제거하였습니다.

td$Job <- as.factor(td$Job)

td$Other_debtors_guarantors <- as.factor(td$Other_debtors_guarantors)

td$Other_installment_plan <- as.factor(td$Other_installment_plan)

td$Personal_status___sex <- as.factor(td$Personal_status___sex)

td$Property <- as.factor(td$Property)

td$Purpose <- as.factor(td$Purpose)

td$Saving_accout <- as.factor(td$Saving_accout)

td$Present_employment <- as.factor(td$Present_employment)

vd$Job <- as.factor(vd$Job)

vd$Other_debtors_guarantors <- as.factor(vd$Other_debtors_guarantors)

vd$Other_installment_plan <- as.factor(vd$Other_installment_plan)

vd$Personal_status___sex <- as.factor(vd$Personal_status___sex)

vd$Property <- as.factor(vd$Property)

vd$Purpose <- as.factor(vd$Purpose)

vd$Saving_accout <- as.factor(vd$Saving_accout)

vd$Present_employment <- as.factor(vd$Present_employment)그리고, 범주형 변수의 자료형을 factor로 변경해줍니다.

# Logistic regression

log_reg <- glm(Credit_status ~., data=td, family=binomial(link='logit'))

summary(log_reg)

Call:

glm(formula = Credit_status ~ ., family = binomial(link = "logit"),

data = td)

Deviance Residuals:

Min 1Q Median 3Q Max

-2.60569 -0.76238 0.01414 0.81211 2.62490

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) 3.920e+00 1.643e+00 2.386 0.01704 *

Checking_account -6.406e-01 1.202e-01 -5.331 9.76e-08 ***

Duration_in_month 1.862e-02 1.459e-02 1.277 0.20177

Credit_history -4.767e-01 1.469e-01 -3.244 0.00118 **

Purpose1 -1.408e+00 5.777e-01 -2.437 0.01482 *

Purpose2 -7.180e-01 3.822e-01 -1.879 0.06027 .

Purpose3 -1.063e+00 3.760e-01 -2.828 0.00468 **

Purpose4 -9.854e-01 1.371e+00 -0.719 0.47237

Purpose5 5.973e-01 8.213e-01 0.727 0.46707

Purpose6 5.610e-01 7.357e-01 0.762 0.44576

Purpose8 -1.578e+00 1.383e+00 -1.141 0.25371

Purpose9 -2.887e-01 5.231e-01 -0.552 0.58098

Purpose10 -2.437e+00 1.019e+00 -2.391 0.01682 *

Credit_amount 1.693e-04 6.977e-05 2.426 0.01527 *

Saving_accout2 -4.907e-01 4.437e-01 -1.106 0.26875

Saving_accout3 1.104e-01 5.999e-01 0.184 0.85395

Saving_accout4 -1.528e+00 7.421e-01 -2.058 0.03956 *

Saving_accout5 -7.697e-01 3.633e-01 -2.119 0.03412 *

Present_employment2 3.981e-01 6.296e-01 0.632 0.52721

Present_employment3 5.070e-01 5.964e-01 0.850 0.39527

Present_employment4 -2.849e-01 6.610e-01 -0.431 0.66646

Present_employment5 4.859e-01 6.178e-01 0.786 0.43159

Installment_rate 3.341e-01 1.311e-01 2.548 0.01083 *

Personal_status___sex2 2.157e-01 5.930e-01 0.364 0.71604

Personal_status___sex3 -6.707e-01 5.716e-01 -1.173 0.24065

Personal_status___sex4 7.366e-01 6.816e-01 1.081 0.27986

Other_debtors_guarantors2 3.906e-01 5.656e-01 0.691 0.48985

Other_debtors_guarantors3 -1.818e+00 6.286e-01 -2.893 0.00382 **

Present_residence -1.289e-01 1.360e-01 -0.948 0.34334

Property2 4.195e-01 3.761e-01 1.115 0.26477

Property3 2.553e-01 3.531e-01 0.723 0.46965

Property4 5.527e-01 5.082e-01 1.088 0.27678

Age -1.066e-02 1.414e-02 -0.754 0.45088

Other_installment_plan2 -2.085e-01 7.125e-01 -0.293 0.76979

Other_installment_plan3 -1.116e+00 3.981e-01 -2.804 0.00505 **

Housing -8.794e-02 2.958e-01 -0.297 0.76625

Num_of_existing_credits 4.591e-01 2.641e-01 1.738 0.08218 .

Job2 -6.112e-02 1.090e+00 -0.056 0.95527

Job3 -3.324e-01 1.050e+00 -0.316 0.75162

Job4 -1.382e-02 1.065e+00 -0.013 0.98964

Num_of_people_liable 2.750e-01 3.711e-01 0.741 0.45860

Telephone -1.327e-01 3.061e-01 -0.434 0.66455

Foreign_worker -1.449e+00 7.526e-01 -1.925 0.05421 .

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 582.24 on 419 degrees of freedom

Residual deviance: 410.88 on 377 degrees of freedom

AIC: 496.88

Number of Fisher Scoring iterations: 5glm 함수를 통해 로지스틱 회귀를 적합할 수 있습니다.

summary를 통해, 각 변수의 유의성 또한 알 수 있습니다.

log_reg$fitted.values <- ifelse(log_reg$fitted.values > 0.8,'Y','N')

misclassification_train <- mean(log_reg$fitted.values != td$Credit_status)

misclassification_train

[1] 0.32380950.8의 값을 threshold로 지정하고, 오분류율을 계산해보았습니다.

약 32%에 해당하는 관측치들이 오분류가 되었네요.

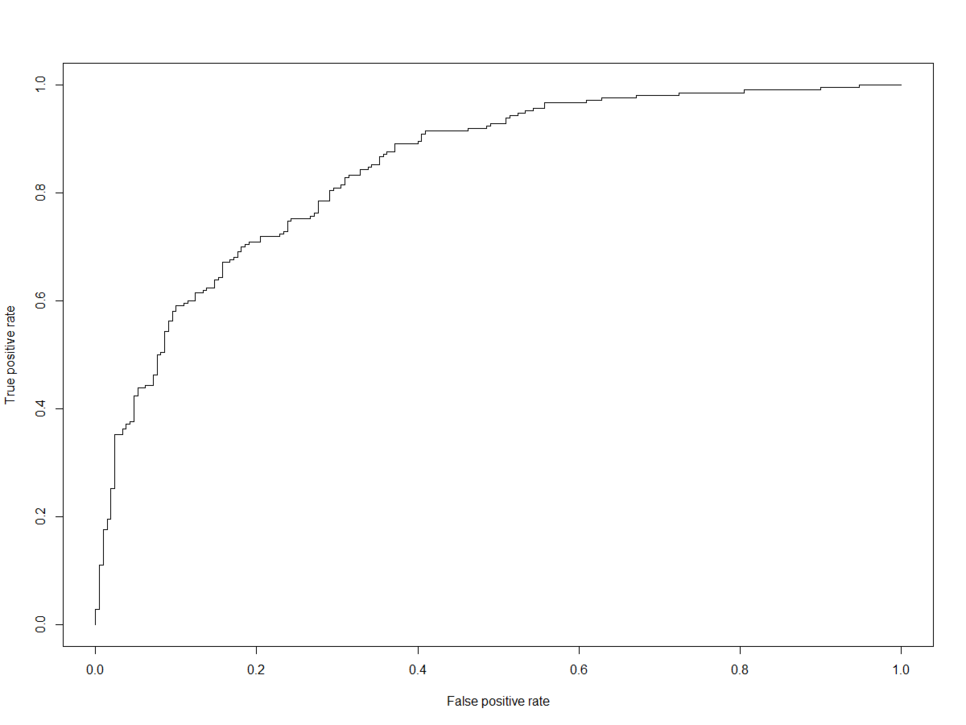

library(ROCR)

log_reg <- glm(Credit_status ~., data=td, family=binomial(link='logit'))

p <- log_reg$fitted.values

pr <- prediction(p, td$Credit_status)

prf <- performance(pr, measure = "tpr", x.measure = "fpr")

plot(prf)

ROCR 패키지를 통해 ROC 곡선을 그릴 수 있습니다.

auc <- performance(pr, measure = "auc")

auc <- auc@y.values[[1]]

auc

[1] 0.8450794ROC 곡선 아래의 면적인 AUC를 계산할 수 있습니다.

0.845로 굉장히 높은 값이 나왔네요.

fitted.results <- predict(log_reg,newdata=vd,type='response')

fitted.results <- ifelse(fitted.results > 0.8,'Y','N')

misclassification_valid <- mean(fitted.results != vd$Credit_status)

misclassification_valid

[1] 0.3611111마지막으로, Test 데이터셋에 대한 오분류율도 확인해보았습니다.

'데이터 다루기 > Base of R' 카테고리의 다른 글

| [R] 연관성 분석 (Association rule) (0) | 2020.04.19 |

|---|---|

| [R] Decision Tree (의사결정나무) (0) | 2020.04.09 |

| [R] K-nearest neighbor (KNN) method (0) | 2020.04.07 |

| [R] Hierarchical clustering, K-means clustering (0) | 2020.03.16 |

| [R] Principal Component Analysis (PCA), Factor Analysis (0) | 2020.03.11 |